Miami International Deep Dive

Miami International ($MIAX): A 51% Margin Toll Road With Free Call Options Attached

Introduction

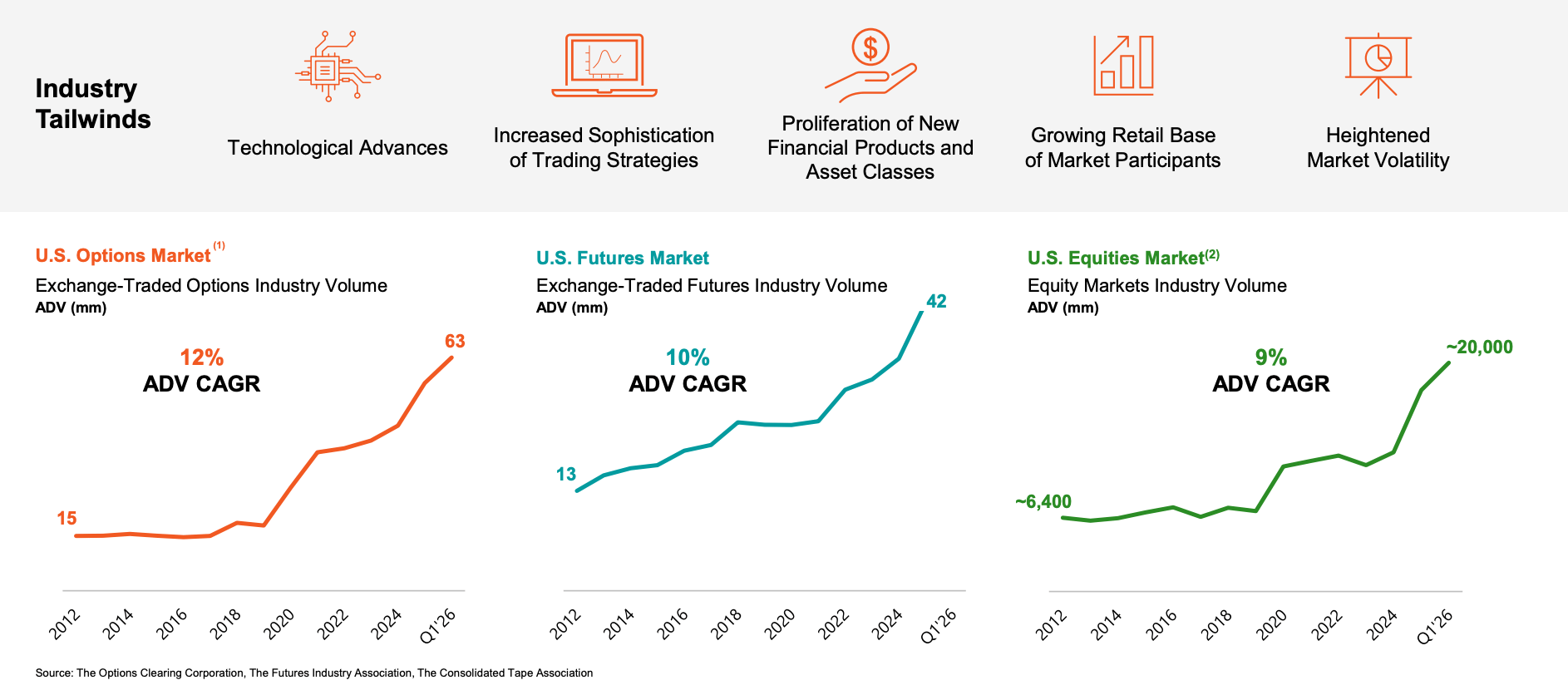

Prediction markets stopped being a curiosity a while ago. Tens of billions of dollars now move through contracts on elections, rate decisions, earnings, and sports. The contracts look like stocks and settle like futures, and the platforms running them have become some of the most talked-about names in finance. Kalshi and Polymarket are household words on trading desks and group chats alike. Robinhood has pushed event contracts to millions of retail accounts and routes enormous volume into the category. The land grab is not coming. It is here, it is loud, and the firms building the rails beneath it are being valued at billions.

Here is what almost nobody has noticed. One of the more valuable positions in that whole land grab does not sit inside a venture fund or a crypto wallet. It sits on the balance sheet of a profitable, fast-growing, publicly traded exchange operator, carried at cost, with management telling analysts to exclude it from their models. The company sold 90% of a CFTC-licensed exchange and clearinghouse to a venture built by Robinhood and Susquehanna, booked a $50 million gain in the process, and kept 10% of the upside for free. While everyone argues about Kalshi’s valuation, this stake is invisible to most screens in the market.

That company is Miami International Holdings, and the prediction-market stake is the loudest example of how badly it is understood. It is also deliberately not the reason to own it.

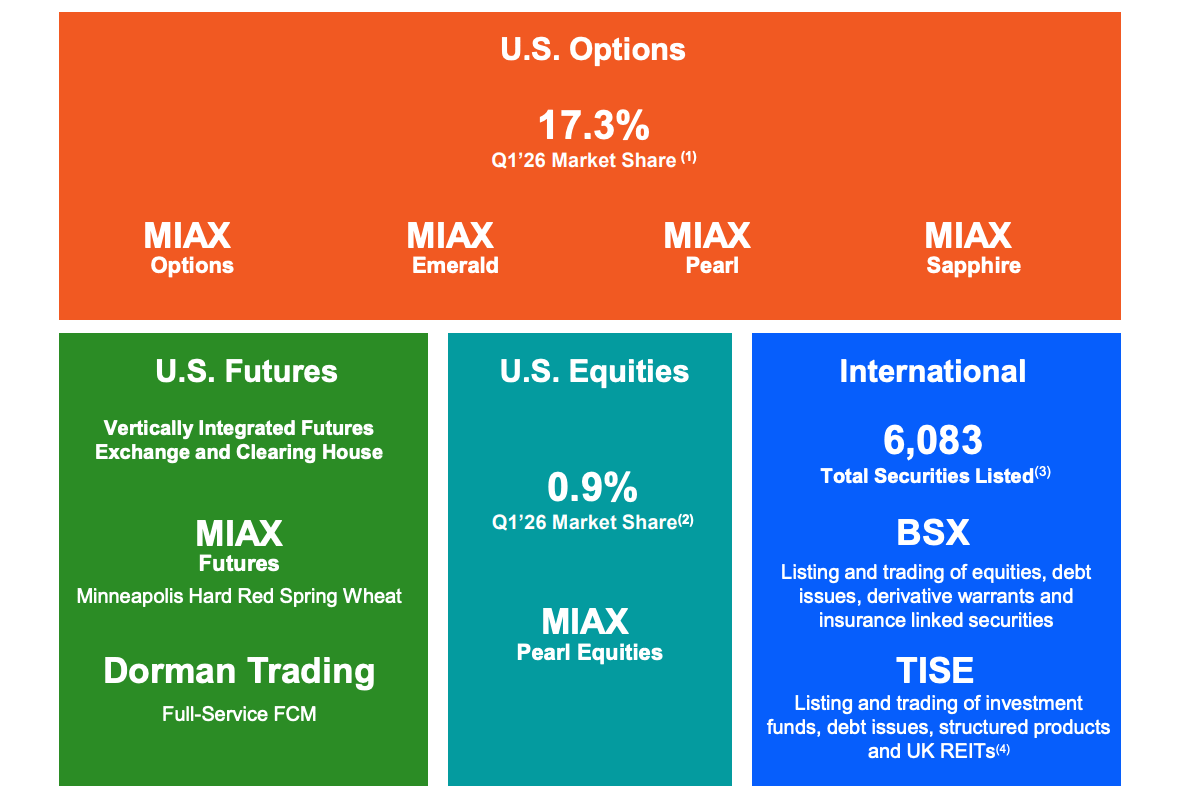

MIAX runs 8 exchanges across US options, equities, futures, and international listings. It went public in August 2025 at $23 and ran pretty hard on its first day. It trades near $41 today, with a market cap of around $3.9 billion. The consensus files it as a small, 4th-place options venue that caught a volatility spike, is now slowing down, and has a Nasdaq lawsuit hanging over it.

Here is what I think most are missing. Underneath the trading volume everyone fixates on sits a recurring, 51% margin business that grows whether or not a single contract trades that day, and the market is pricing it as if it were the cyclical flow on top. Stacked on that core is the only structurally defensible attack anyone has built on the SPX and VIX options complex, the most profitable franchise in the exchange industry, which Cboe has defended without a scratch for 40 years. And wrapped around all of it is a stack of assets the market literally cannot see because they are carried at cost and modeled by no one, with the prediction-market stake being merely the most obvious.

Peter Thiel asks what important truth very few people agree with you on. Here it is in one line: the interesting question about MIAX is not its market share or its daily volume, the things every analyst already models to death. It is whether the company has quietly assembled a structural position that competitors cannot copy, and whether the market is paying for it. The answer to the first is yes. The answer to the second is no. That gap is the entire trade.

The duopoly attack is real but unproven. The single most important product has not launched yet. The lawsuit is a coin flip you cannot hedge. And the board just lost the director who believed in it most. Each gets its due below. What is left after all of it is a quality compounder priced like a slow one, with a basket of free call options stapled to the side.

The Toll Road Under the Volumes

An exchange earns two kinds of money, and the market only watches one of them. Transaction revenue is the per-contract fee charged when a trade prints. It rises and falls with volatility. It’s what every analyst models off industry volume, and it is genuinely cyclical. Non-transaction revenue is the quiet one. It’s what firms pay simply to connect to the exchange, to pull their data, to hold a port, to keep a presence on the network. They pay to be in the building, not to do anything once inside. It looks far less like trading and far more like a software subscription, and it is the part of MIAX that the market refuses to price correctly.

In Q1 2026, that subscription bucket grew 45% year over year. Access fees, the charges to connect, rose 38.5% to $33.4 million. Market data rose 34.4%. The CFO laid out the access-fee growth precisely: roughly half from new member connections, half from pricing, with the pricing half split between a January 1 fee increase and the expiration of waivers on the new Sapphire exchange. None of these moves has a daily volume. A firm wired into MIAX pays in a dead tape and a screaming one alike.

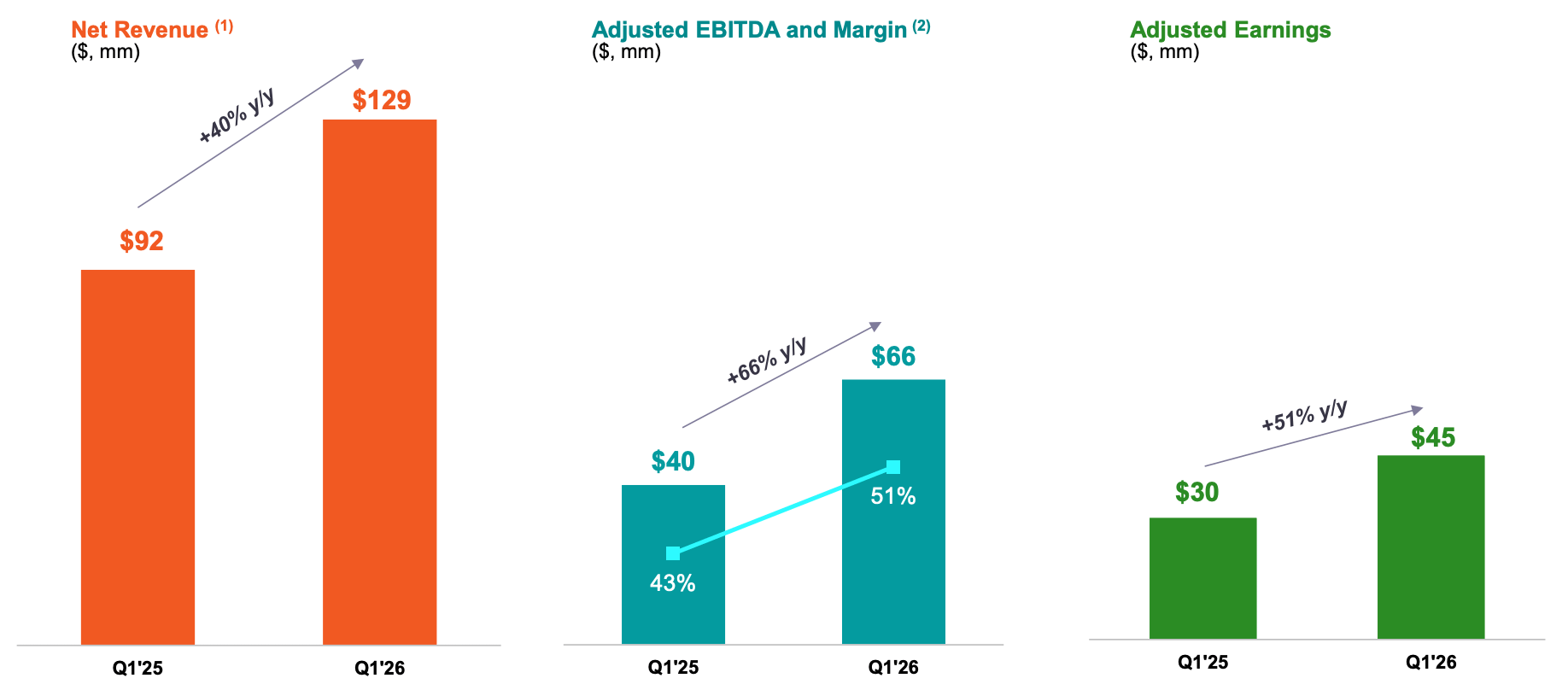

That is where the margins come from, and they are the tell. An exchange is a fixed-cost machine: the technology is built, the data center hums, and the regulatory staff is hired. Every incremental dollar of connectivity and data falls to the bottom line at almost no added cost. Q1 adjusted EBITDA margin hit 51%, up 800 basis points year over year, on $128.6 million of net revenue, while adjusted EBITDA itself grew 66% to $66.1 million. Adjusted earnings rose 51% to $45 million. Adjusted EPS of $0.42 beat the Street’s $0.36. Operating income doubled to $46 million. This is what operating leverage looks like when recurring revenue scales over a cost base that barely moves, and it is accelerating.

Sapphire is a tailwind hiding in the footnotes. When MIAX launches a new exchange, it waives connection fees to pull members on, then removes the waivers over time, exactly as it has done with every venue before. The members did not leave when the trial ended. They are converting to paying connections, which means a meaningful slice of the growth is not a one-time event but the leading edge of a multi-quarter repricing as the remaining waivers roll off. Free to acquire, then monetize the installed base. That is the software playbook, run by an options exchange that the market still values like a volatility bet.

An honest adjustment, the 45% headline is flattered by the June 2025 TISE acquisition and by a single $2.7 million ad hoc historical data sale that management explicitly told investors not to model as a run rate. Strip both, and the organic growth lands around 32%. Lower than the headline. Still elite for a business compounding at a 51% margin.

The toll road is not the exciting part of this story. It is the part that means you do not need the exciting parts to avoid losing money.

The Trading Business Is Better Than Its Reputation

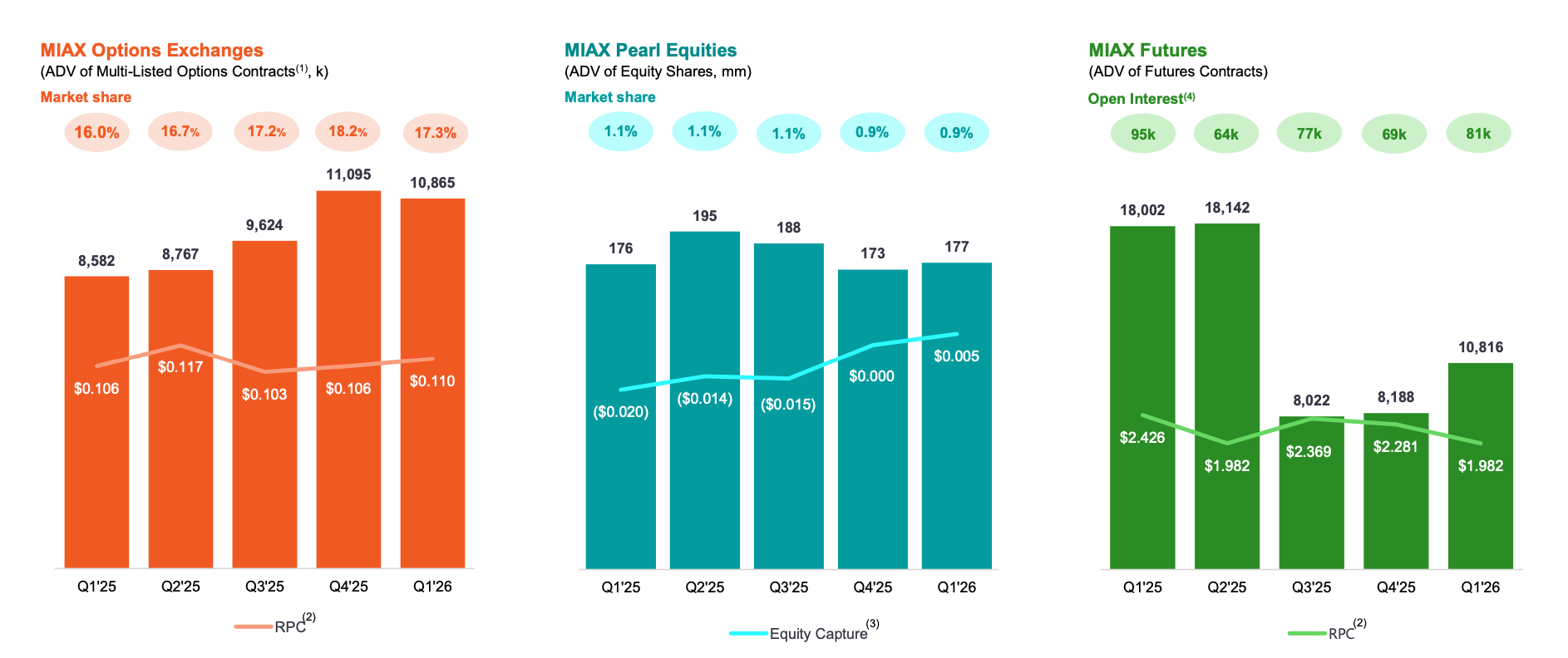

MIAX held 17.3% of US multi-listed options share in Q1, up from 16.0% a year earlier. Average daily volume grew 27% versus the industry’s 17%, indicating it is taking share as the pie expands. Revenue per contract rose 3.8% to $0.110. From a standing start in 2012, this company built the 3rd-largest options franchise in the United States, growing organic average daily volume from 1.0 million contracts in 2015 to 6.7 million in 2024, a 23.5% annual clip. That is not a flash in a volatile quarter. That is a 9-year compounding machine.

The bear case grabs one fact and runs: share slipped sequentially from the prior quarter. Late entrant peaks, incumbents push back, the story writes itself. Except that is not what happened, and management said so flatly. The sequential dip was deliberate. MIAX shed low-capture and negative-capture volume, the order flow that pads a share headline while earning the exchange little or actively costing it money to attract. What it grew was the high-quality flow: complex orders, high-touch business through the Sapphire floor, and single-name weekly options. Headline share ticked down a hair. Revenue per contract went up. That is an owner pruning junk, not a franchise losing ground, and a market that, when it scores exchanges on share-of-volume headlines, mistakes the one for the other.

Look at where the quality flow is going, because this is the near-term growth lever nobody is modeling. In the 9 single-name weekly classes, MIAX runs at 18% to 20% share, well above its 17.3% company average, and management’s own words for the launch were that it is off to the races. These are the highest-capture, highest-quality classes the exchange trades, and because its share there is highest, MIAX tends to win the new listings as the program expands. The industry is actively debating whether the next wave comes from adding Tuesday and Thursday expirations or from adding more names. Either way, the volume grows, and MIAX is positioned to take more than its average share.

The Sapphire floor is the same story in physical form. Trading-floor share across the industry rose from 6.5% in 2025 to 8.1% in Q1 2026, and MIAX’s own piece of floor volume roughly doubled from about 5% to about 10%, with new brokers and market makers still joining and new functionality shipping through the year. Floor business is complex, high-touch, high-capture flow, the opposite of the commoditized electronic volume that bears assume defines this company. The floor is gaining share, not bleeding it, and it is the highest-quality share in the building.

The equities segment is a quieter proof of the same discipline. Net revenue grew 82% to $6.7 million, and capture flipped from inverted, meaning MIAX was paying for flow, to net positive, with the segment loss shrinking from $4.0 million to $1.1 million. A business that used to pay to attract orders now gets paid for them. That is management optimizing for economics over vanity, showing up in a second segment.

One segment is genuinely ugly, and there’s no hiding it. Futures lost money. Q1 futures net revenue fell 21% to $4.6 million, with a $12.4 million operating loss and negative $8.6 million adjusted EBITDA, hit by the timing of migrating participants onto the new in-house Onyx platform, softer commodity volatility, and lower revenue per contract from new incentives. It is a real drag today. It is also the launch pad for the most ambitious thing this company is attempting, which is the entire reason the loss exists. MIAX is bleeding in futures because it is spending to build something far larger on top of it.

The Duopoly Nobody Has Cracked in 40 Years

About 95% of all US index options volume sits in 2 products: SPX, the S&P 500 option, and VIX, the volatility option. Both belong to Cboe. SPX recently set a record share even within the universe of S&P-500-linked derivatives, with average daily volume above 4.5 million contracts. This is not a competitive market with a leader out front. It is a monopoly nested inside a monopoly, and it is the single most profitable franchise in the exchange industry, because index options are cash-settled, high-priced, and stickier than any other product class in trading. If you can take even a sliver of it, the economics dwarf anything in multi-listed equity options.

Many have tried. None have succeeded, and the reason is a self-feeding network effect. Traders go where liquidity already is because depth means tighter spreads and the ability to move real size, and liquidity pulls in more liquidity. You cannot build a better mousetrap because the mousetrap is not the product. The product is the pool of other traders already standing in the room. When the International Securities Exchange tried to list competing S&P products last decade, Cboe did not out-trade it. Cboe sued and won because it holds an exclusive license to the S&P 500 that runs through 2032. A 2010 ruling barred ISE from listing the products and barred the clearinghouse from clearing them. The moat is liquidity wrapped in a license you cannot buy at any price.

So you do not attack the license. You go around it. MIAX did two things that together create a position the incumbents cannot copy.

First, it licensed Bloomberg’s indices, the Bloomberg 500 and Bloomberg 100, on a 10-year exclusive. Same large-cap US exposure as the S&P 500 and Nasdaq 100, built differently. Where S&P leans on a committee to decide membership, a discretionary process with delays, Bloomberg uses a transparent, rules-based algorithm. Constituents enter and exit on fixed criteria, and newly public companies get admitted fast, where a committee drags its feet. With the largest IPO pipeline in a generation about to hit, that speed is the feature, not a footnote. And the Bloomberg license has nothing to do with the S&P exclusivity, so there is no 2032 injunction waiting for a product that Cboe does not own the rights to.

Second, the move almost nobody is discussing, and the one that matters more. MIAX clears these futures at the Options Clearing Corporation. In May 2026, MIAX Futures became OCC’s 5th participant exchange. That reads like plumbing. It is the whole game. Because the products clear at OCC, the same clearinghouse behind the entire US-listed options market, a trader can cross-margin a Bloomberg index position against existing OCC-cleared options. Capital that would otherwise sit trapped against two separate positions nets into one. For a professional trading firm, capital efficiency is not a convenience. It is the difference between a product worth trading and one that is dead on arrival.

This is the part the incumbents cannot mirror. Cboe clears its index futures at its own captive clearinghouse. CME clears its equity futures at CME. Their entire model depends on owning the clearing and keeping the margin inside their own walls. They cannot let a trader net against a rival’s products without dismantling the vertical integration that prints their money. MIAX has no clearinghouse to protect, so it has every incentive to maximize cross-margin efficiency for the trader. The edge is not a feature MIAX bolted on. It is a structural consequence of being the attacker, and it is the exact move the incumbents are least able to copy without cannibalizing themselves.

There is a second structural argument, and it comes from the executive running the product. Shelly Brown, who built MIAX Futures and spent 35 years in this industry at PEAK6, Nasdaq, and Susquehanna, argues that index options do not require a trading floor at all. The incumbent keeps its floor open because it always has and because its members are there, but a fully electronic index market means the floor and electronic market makers stop competing with themselves, which tightens spreads and shows more liquidity on screen. The incumbent also caps electronic complex orders above a certain size and pushes them to the floor. MIAX intends to automate exactly those functions. A product that is better on the screen, cleared in a way that frees up capital, on an index the incumbent does not control.

A rules-based index Cboe does not own, cleared through the one venue that lets traders net it against everything else they hold, offered electronically by the one player whose business model is not threatened by that netting. If you set out to design the only defensible way to attack SPX, this is what it would look like.

Why This Is Hard, and Why That Is the Point

Now I’ll argue against myself because the difference between this and a press release lies in the next few paragraphs.

There is a clean line between an integration problem and a physics problem. An integration problem is hard but bounded: assemble known parts, wire them together, and ship. MIAX has solved that completely. The technology is built, Bloomberg is signed, OCC is wired in, and the products are launching on schedule. That is a genuine achievement, and it is done.

Displacing entrenched liquidity is the physics problem. You cannot engineer a deep order book or pay your way to durable open interest, at least not for long. You have to convince traders to leave a pool where everyone else already stands and walk into an empty room, before there is any liquidity there to attract them. That is the constraint that beat everyone who came before, and it does not care how elegant your index methodology or your clearing structure looks on a slide.

The early data says exactly that, and it is the most important fact in this report. MIAX launched its first Bloomberg product, the Tini Bloomberg 100 future, in mid-May. Launch-day volume was strong, roughly 24,700 contracts on the first full day, where a skeptic would have guessed a few hundred. But drop one level. At the close of that same day, open interest, the positions actually held overnight, was 197 contracts. The following days: 150, 116, 264. Nearly 24,700 contracts changing hands, fewer than 200 held. That is not end-user demand. That is market makers passing inventory back and forth intraday, almost certainly seeded by launch incentives, and going home flat. Manufactured liquidity, not adoption.

And the product that matters most has not launched. The cash-settled Bloomberg index options, as opposed to the futures, are where the real SPX and VIX economics live. Options are the high-margin, sticky, profitable class. Futures are the warm-up act. The SEC approved the B500 options back in May 2025, but MIAX has not listed them yet, citing business reasons, and chose to launch futures first. The whole thesis ultimately rests on the options. The S-1 is guided to a first-half-2026 launch. We are at the edge of that window with futures live and options still on the shelf.

So underwrite it as a call option, not a fact. The strike is the cash-settled options launch. The signal that tells you it is going in the money is not volume, it is open interest. Anyone can buy a volume headline on launch day with rebates. Nobody can fake durable open interest because it reflects traders choosing to leave their money in your product overnight. If, 2 or 3 quarters after the options launch, open interest is building into the tens of thousands of contracts, the impossible is happening, and the stock is worth a multiple of today’s price. If it keeps dying to near zero every night, the physics won, the way it always has, and the option expired worthless. Watch the open interest. Ignore the volume. It is the single cleanest tell in the entire thesis.

And Cboe is not asleep. On its last call, record revenue of $728.9 million and SPX at all-time highs, management addressed competition for the SPX franchise ahead of 2032 and called its ecosystem of floor and electronic liquidity intentional and difficult to replicate. It did not name MIAX. It did not have to. The incumbent is enormous, entrenched, and profitable enough to defend itself however it chooses. The window MIAX is attacking through is real. It is also narrow, and it will not stay open by default.

The Options the Market Cannot See

Everything to this point justifies owning MIAX as a quality compounder at a fair price. What makes it asymmetric is the stack of things you get for nothing, because they sit at cost, generate no modeled revenue, and are therefore absent from every spreadsheet. The discipline, the same one that protects the rest of the case, is that none of these is required. If every one of them goes to zero, the core still carries the stock. They are upside, not foundation.

Rothera, the prediction-market stake

In January 2026, MIAX sold 90% of its CFTC-regulated futures exchange and clearinghouse, formerly LedgerX, to a venture backed by Robinhood and Susquehanna and booked a $50 million gain. The business was renamed Rothera. MIAX kept 10%, carried at cost, with future distributions flowing through as income. Management said plainly that it should not be in anyone’s model. Long-term optionality, nothing more, in their own framing.

It is a real option because of how the venture is built: a 3-legged stool, each leg hard to assemble. Robinhood brings the largest retail distribution funnel in prediction markets. Susquehanna, one of the best derivatives market-making firms in the world, brings liquidity, the exact thing these markets live or die on. And the old LedgerX brings live CFTC licenses as a designated contract market, clearinghouse, and swap execution facility, rails that take years to build and cannot be willed into existence. Retail reach, professional liquidity, and a federal license, assembled into one venture, in the fastest-growing new market in finance. MIAX got paid to build it and kept a tenth of the upside at no ongoing cost.

Now the discipline, because this is where a careless writer overreaches and a skeptic pounces. This is not the main reason to own the stock. It is 10% of an early venture, in a category where Robinhood already routes enormous volume through a competitor, Kalshi, which fairly raises the question of how committed it is to its own joint venture. For the stake to move a $4.5 billion company materially, the venture would need to reach a $10 billion valuation, so that 10% is worth $1 billion. Possible in a world where prediction markets go fully mainstream. A moonshot, not so much a base case. Hold it the way management books it: at cost, a free option, the downside already paid for by the gain on the sale, and the upside uncapped. You are not paying for the lottery ticket. It came in the box.

Pyth, Onyx, and the international venues

MIAX holds 250 million locked Pyth tokens that unlock in May 2026 and May 2027, carried as a derivative asset of around $8 to $9 million. Small against the market cap, and it whipsaws GAAP earnings through mark-to-market, but it’s a real asset that the market backs out and forgets.

Onyx is MIAX’s in-house trading platform, the same stack it has used to migrate every venue it has acquired onto its own rails. The bull story is that it is licensing it to other exchanges as high-margin software. Precisely, there is no third-party Onyx licensing business today and no signed deals. Pure optionality. The market pays nothing for it because there is, for now, nothing to pay for. If that changes, it is upside. Today, it is a maybe, and I personally view it as a maybe.

TISE and BSX are two international venues most US investors have never heard of. The International Stock Exchange, acquired in June 2025, is a leading European professional bond market with 4,500+ securities, the largest venue for UK real estate investment trusts, structured so that debt issuers can list quickly and tax-efficiently outside the reach of EU directives. The Bermuda Stock Exchange leads the world in insurance-linked securities, tens of billions outstanding, plus digital-asset listings under Bermuda’s crypto framework. The international segment grew net revenue almost 6x to $5.6 million and turned EBITDA-positive, and MIAX is now streamlining sales across the two to chase global debt and listings clients. Small today. Recurring listing-fee annuities plus genuine regulatory optionality, the ability to list products that are hard or impossible to bring to market onshore. Another free option in the model.

The Nasdaq Lawsuit

Every honest thesis has its own tail risk. Here is MIAX’s, unsoftened.

Nasdaq sued MIAX in 2017 in federal court in New Jersey over electronic trading technology, alleging patent infringement and trade secret theft. The patent half collapsed: the patents were invalidated, and those claims dismissed with prejudice by 2022. The trade-secret claim survived. In September 2025, the court denied both sides’ motions for summary judgment and sent the case to a jury in a single trial with 2 phases: Nasdaq’s claims first and MIAX’s counterclaims second, including fraud on the patent office and antitrust theories.

Here is the part I cannot resolve. The damage number is sealed. The summary-judgment opinion was filed under seal for redactions. MIAX takes no reserve and discloses no estimate, saying only that it cannot predict the outcome and that an adverse result could be material. Nasdaq has characterized the surviving claim as capable of a substantial award. A real jury trial, a live claim, no public number, no fixed trial date. An unhedgeable coin flip, and anyone handing you a precise probability is guessing. The litigation is already showing up in the numbers, with legal expenses up $1.7 million in the quarter, a cost that will continue until this is resolved.

What I can give you is the shape, not a point estimate. MIAX holds over $550 million in cash against less than $2 million of debt, which is what actually determines whether an adverse judgment is survivable, and it is, even at a large number. Trade-secret damages can take the form of the plaintiff’s lost profits, a reasonable royalty, or disgorgement of the defendant’s gains, with the equitable portions usually decided by the judge rather than the jury, which adds uncertainty about the method. Treat the risk as a discrete event with a fat tail, size the position accordingly, and watch the docket for 2 things: the unsealed opinion, which finally puts a number in public view, and a trial date. Either one moves the stock in either direction.

A real risk. On this balance sheet, not an existential one. But it is the thing that can go wrong that you cannot hedge.

The Anchor Shareholder, and the Empty Seat

The ownership register says something the income statement cannot. Horizon Kinetics, the deep-value, long-duration firm, owns 12.1% of MIAX, a position it began with near 10.7% and roughly $65 million of client capital at the IPO, and has since added to. This is not a momentum fund renting a quarter of price action. It is a hold-for-a-decade shop, and a stake that size in a newly public exchange is the signal long-duration capital sends when it believes it has found a compounder the market has yet to figure out.

And here is the loss, because it belongs in the same breath. Murray Stahl, Horizon Kinetics’ co-founder and chief investment officer and a MIAX director, the loudest believer on the board, died suddenly in April 2026. Stahl personally held millions of shares, a real slice of his own portfolio, and had been buying in the open market in the months before he died. On the Q1 call, Gallagher noted that one of the things Stahl believed was that there was a real opportunity for a truly global exchange operator, which is precisely the international thesis the TISE and BSX venues are quietly building toward. His conviction was not abstract. It was his own capital, repeatedly, near these prices, behind a specific vision that the company is still executing.

Succession transferred control to two of his longtime partners, and Horizon Kinetics retains a board seat, which supports continuity in the position. But it would be dishonest to call the loss immaterial. The board lost the name that most validated the long-term thesis to the outside world. Watch one thing, mechanical and unambiguous: any filing showing Horizon Kinetics trimming the stake removes the most important conviction anchor under the stock and is a signal. Holding or adding is confirmation. For now, the anchor holds, but the hand that set it is gone.