Ouster Deep Dive

Ouster ($OUST): The Eyes of the Robot Economy

Two notes before the work starts.

Vantix Research now has a Discord server, and it is open to all paid subscribers. Link your Substack and Discord accounts to join.

And a real debt is owed to @usppdd on X. A large share of the partnership threads mapped in this piece started as a sighting, a photo, or a post on that account before they were run down to primary sources here. The lead generation was theirs. Credit where it is due.

Now, the company.

Introduction

For seventy years, automation lived behind a fence.

Machines were blind. They sat bolted to a factory floor, repeating one motion inside a cage, because a blind machine cannot be trusted to perceive anything outside the line painted around it. That arrangement is ending, and not gradually. Today, haul trucks the size of houses drive themselves across open-pit mines. Forklifts thread pitch-dark warehouse aisles with no one aboard. Full-size buses run scheduled public routes through European cities with an empty driver’s seat. Tractors work fields alone, inspection drones crawl through sewers and volcanic lava tubes, twenty-thousand-container ships steer themselves across oceans, and humanoid robots walk the floors of Fortune 500 warehouses on their own two legs. NVIDIA, whose chips run most of it, has a name for this: Physical AI, the wave that comes after the chatbots, and the company frames it as the largest market it has ever set out to serve. The entire installed base of moving machines on earth, rebuilt to operate with no human inside.

Every one of those machines has the same first problem. Before it can think, it has to see, and not the way a phone sees, flat and inferring depth from a guess. A two-hundred-ton truck, or a robot working an arm’s length from a person, has to know, to the centimeter and in real time, where every object around it is located in three dimensions. It has to know this in the dark, in dust, in fog, in the glare off wet asphalt at sunset, in exactly the filthy conditions where the most valuable autonomy lives and a camera goes blind. That is a physics problem before it is a software problem. The instrument that solves it, that measures the shape of the world directly instead of estimating it, is lidar.

Here is the part that does not fit the story that almost everyone already believes. The one component the entire robot economy depends on was, as recently as last year, written off as a dead technology.

The self-driving mania of 2021 inflated a dozen lidar startups to billion-dollar valuations on a single promise: that robotaxis were a year out. The year came and went, the robotaxis did not arrive, and the field is a graveyard now. Quanergy filed for bankruptcy. Velodyne, which invented the spinning sensor on the roof of every early self-driving car, vanished into a distress merger. Luminar, the anointed winner, the Tesla supplier whose founder smiled out of every magazine, filed for Chapter 11 this past December. Luminar filed with roughly half a billion in debt against under $200M in assets, while Ouster sits debt-free on ~$175M cash. Tesla called the entire category a fool’s errand from a stage, and the verdict held. One of the companies left for dead fell from a 2021 high near $127 to under $4 a share.

That company sits around $45 today.

The obituary was real. It was also written for the wrong patient. The technology never died. One use of it died, the passenger car, the single market this company abandoned years ago to chase everywhere else, and the machines had begun to move. And everywhere else, it won. The names now running their autonomy on its sensors read like a census of the physical frontier: Komatsu and Sandvik in the mines, Hyundai’s shipyards at sea, John Deere in the fields, Google’s mapping fleet on the streets, Boston Dynamics’ robot dog, the security robot circling the local mall, and a long roster of the humanoid and foundation-model startups NVIDIA itself bankrolls. Most are not American companies. None of them is required to buy American hardware. Cheaper Chinese lidar, in many cases better on paper, sits one purchase order away and is fully legal. They choose the same eyes anyway.

The company is Ouster.

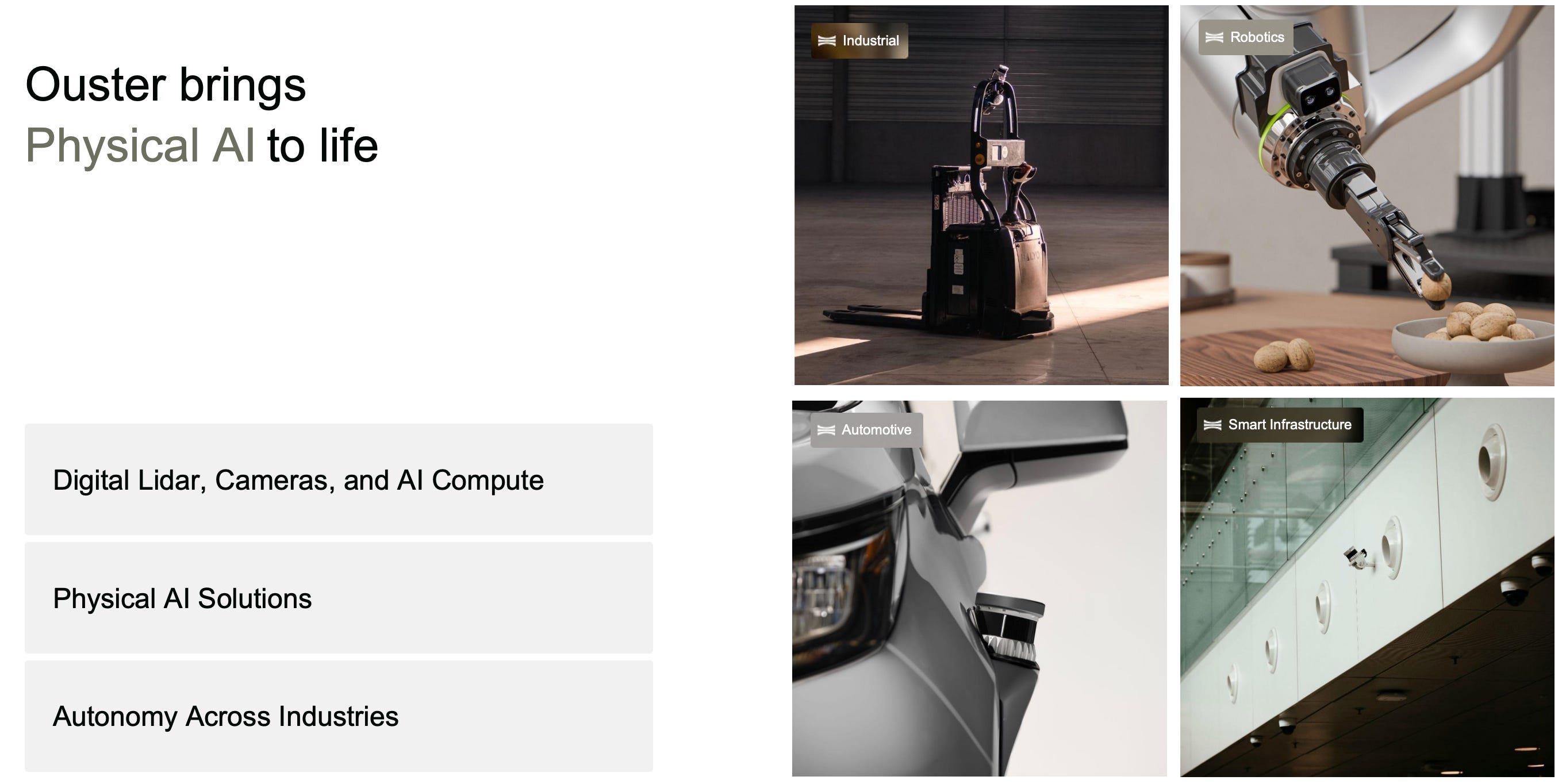

And in three years, it stopped being a company that sells a sensor and became the supplier of an entire layer. Lidar to measure distance. Cameras to capture color and detail. Software to turn the raw torrent of points into something a machine can decide on. One vendor for the whole perception stack of Physical AI.

That is the franchise worth hunting in a buildout this size, not the celebrity robot on the cover, which may or may not be standing in five years, but the layer beneath all of them that gets bought no matter which body wins, the way ASML sits under every advanced chip on earth and is worth more than most of the firms it supplies. Pick the winner of the robot wars, and you might be right. Sell the eyes to every army in the field, and you do not have to be.

So why does a company this well placed still trade where a determined buyer can reach it? Because of the one thing nearly everyone misreads about it. Ouster does not have a moat. It has two, and they are different in kind. The first it earned, in open global combat against cheaper rivals who are, on raw specifications, sometimes better, and that moat pays the modest margins of a hardware business. The second, they did not build at all. Congress built it, a wall of statute that bars Ouster’s most dangerous competitors from the most lucrative rooms in the market, and what Congress grants, Congress can widen, narrow, or let lapse. The first moat is owned. The second is rented. The market, paying close to a software multiple at roughly sixteen times sales, prices both as if they were permanent and the same. They are neither. Separating them is the whole analytical task, and it is the line between a compounding franchise and an expensive lease on a law.

Beneath both sits a third thing that the price ignores completely, because it has not yet appeared in a single line of the financials. Call it the optionality. A hundred and fifty thousand Ouster sensors are already deployed and running, generating the scarcest input in the AI economy, real-world three-dimensional data of the exact kind the world models inside future robots will have to be trained on. A regulatory wall that is American today and could be Western tomorrow, with allied governments studying the same exclusion that the United States already enacted. A platform whose endgame, if it converts, is no longer the sale of hardware at all but a recurring toll on every machine that perceives the world through the stack. None of it is in the price. None of it is promised. All of it is free. The valuation buys the company that exists. The company it could become is thrown in.

This is the rarest setup in the market: an exceptional business whose only real flaw is its price. Which inverts the usual question. The debate is no longer whether Ouster is worth owning, because the evidence below settles it in favor of a company built to keep eating for years. The debate is price and discipline, how to build a position in something this good without handing back the whole prize for a wall no one at the company controls.

What follows earns that answer. A complete map of every customer and partner that could be verified across a dozen frontier industries on three continents. The products, taken apart down to the silicon, including the one breakthrough that may be a true moat and the one feature universally called a moat that is not. The single anonymous customer who quietly pays a third of the bills. The strongest argument against the entire thesis, that robots will never need lidar at all, answered directly rather than dodged. The free options. And the exact prices at which the eyes of the robot economy become cheap enough to own with conviction.

The stock has run. That is acknowledged plainly and priced honestly. But a great machine does not stop being one because the tape got loud, and a name with a beta near four, capable of shedding a fifth of its value in a week on no news at all, is a name that hands patient capital its entry, as long as the work is done and the number is known before it arrives. This is the work.