Pagaya Technologies Deep Dive

Pagaya ($PGY): $3.2 Trillion in Credit Data, 100% Partner Retention, and a Market That Still Doesn't Get It

Introduction

Pagaya Technologies is materializing to become the core infrastructure for consumer lending. When you apply for a personal loan, auto loan, or BNPL financing, there is a good chance Pagaya’s AI is running in the background, deciding whether to approve you.

Here’s how it works:

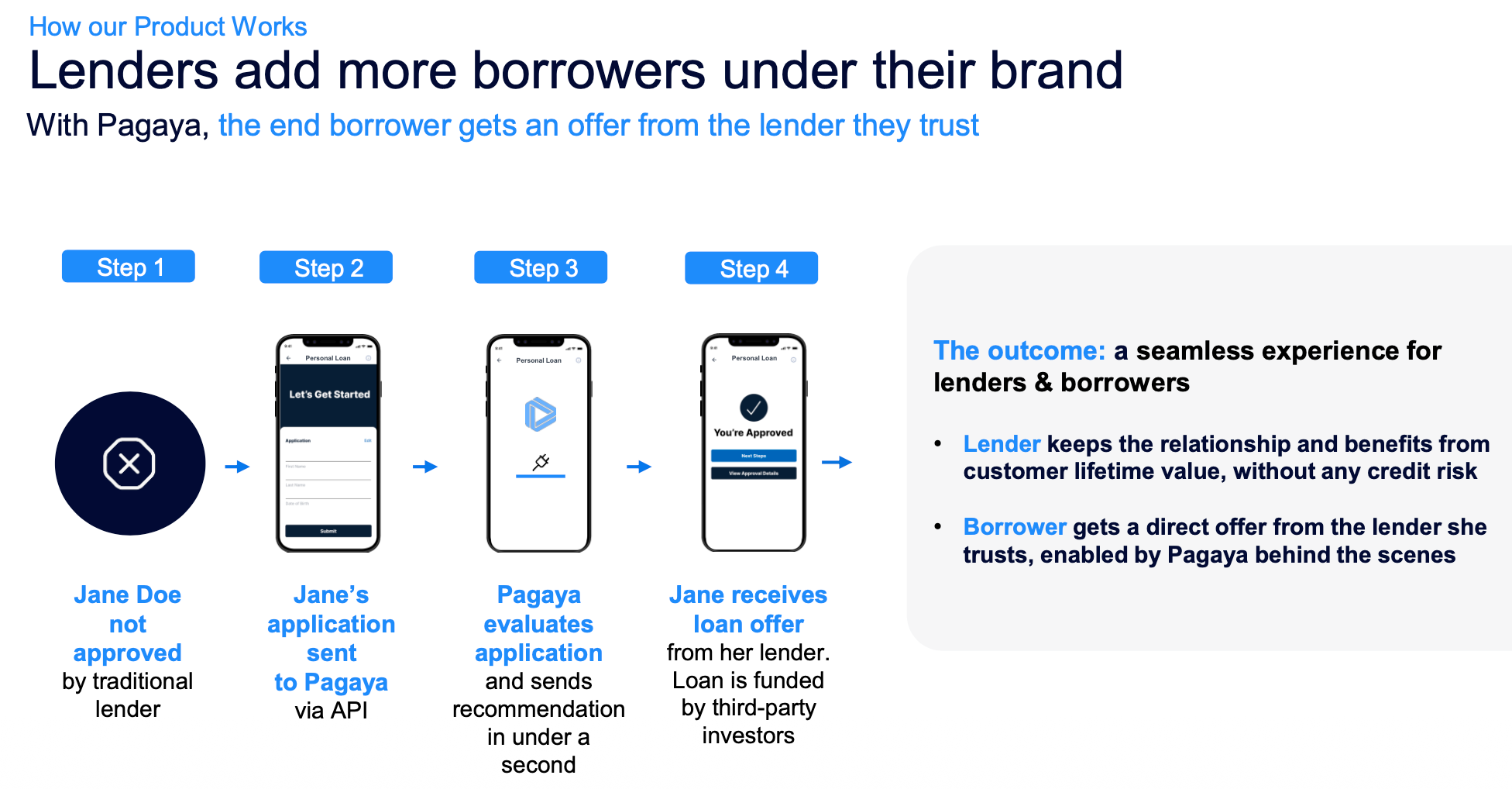

You apply for a loan at a bank or fintech company. The bank’s system reviews your application and declines it (perhaps your FICO score is 680, and they require 700). Before telling you no, the bank’s system automatically sends your application to Pagaya. Pagaya’s AI looks at thousands of data points beyond just your credit score: your cash flow patterns, employment stability, spending behavior, and more.

Pagaya’s AI might then see you as creditworthy and approve you. The loans originated in the bank’s name, but Pagaya immediately buys them and places them with institutional investors.

The consumer never knows Pagaya even exists. The bank earns incremental revenue on a loan it would have probably declined. Institutional investors get access to consumer credit assets, and Pagaya earns a fee on every dollar that flows through its network.

This is why we call it “infrastructure.” Pagaya doesn’t compete with banks, it makes them better. It doesn’t build a consumer brand, it powers other companies’ brands. It doesn’t hold loans on its balance sheet, it places them with investors.

The Problem Pagaya Solves

The 42% Problem

Approximately 42% of US consumers are turned down for credit, even though they can afford to repay. This is not because these people are bad credit risks. It is because traditional credit scoring systems are too blunt to identify them.

Traditional underwriting relies on FICO scores, which use a limited set of variables: payment history, credit utilization, length of credit history, and a few others. These models are designed for consistency and regulatory defensibility.

As a result, a massive population of creditworthy borrowers are declined because they don’t fit the standard mold. Maybe they are young with limited credit history. Maybe they are immigrants with no US credit file. Maybe they are self-employed with irregular income patterns. Traditional systems cannot see past these surface-level issues.

Why Banks Cannot Solve This Themselves

Banks have access to plenty of data and technology. So why don’t they just build better AI themselves?

The answer is structural. Building competitive AI underwriting requires three things simultaneously: proprietary training data across millions of loan outcomes, institutional investors willing to buy AI underwritten loans, and operational infrastructure to handle the origination-to-securitization workflow.

This creates a chicken-and-egg problem. You need data to train good models, but you need good models to generate volume, you need volume to attract investors, and you need investors to fund more volume to generate more data. Pagaya has spent years solving this sequencing problem. A bank starting from scratch would face years of challenges.

More fundamentally, banks do not want to solve this problem themselves. Pagaya’s model generates incremental revenue for banks at zero credit risk to their balance sheets. Why would a bank take on credit risk, allocate capital, and manage complex funding when Pagaya does all of that for them?

How The AI Actually Works

Beyond FICO

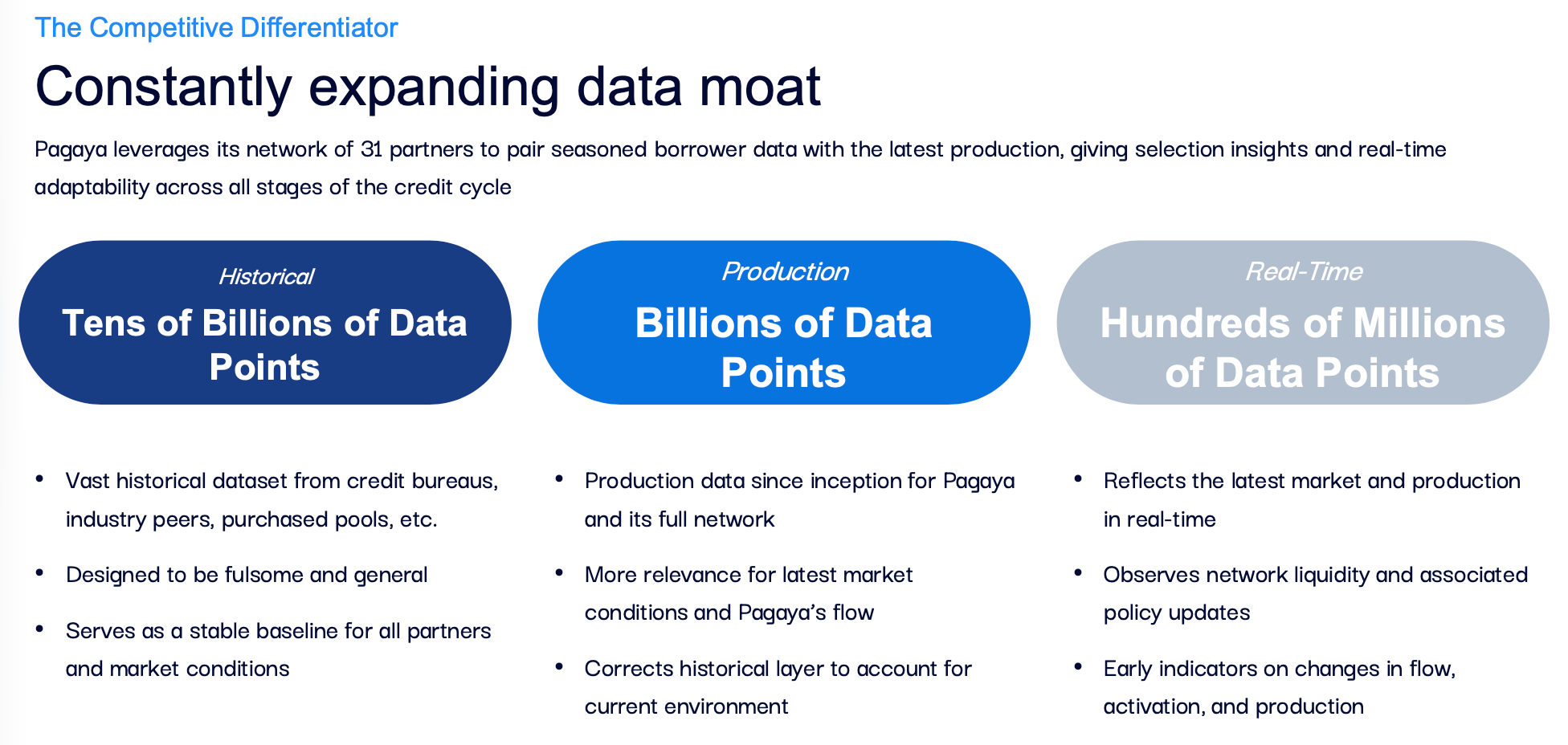

Pagaya’s AI platform has evaluated over $3.2 trillion in cumulative credit applications. Each application feeds thousands of data points into machine learning models that identify patterns human underwriters and traditional scorecards miss.

The AI analyzes variables like cash flow consistency (not just income level), spending patterns and behavioral signals, employment stability indicators, banking relationship depth, and economic trend correlations specific to the borrower’s geography and industry.

This is not magic. It’s pattern recognition at a massive scale. When you have seen 3.2 trillion dollars of applications and tracked how millions of loans actually performed, you can identify subtle signals that predict creditworthiness far better than a three-digit score.

The Data Flywheel

This is where Pagaya’s moat becomes clear. The more applications the AI sees, the better it gets at predicting outcomes. Better predictions attract more partners. More partners generate more applications. More applications improve the AI further. This flywheel has been compounding since 2016.

Importantly, Pagaya trains on data from 31 different lending partners across five asset classes: personal loans, auto loans, POS financing, credit cards, and single-family rentals. This diversity is critical because credit behavior varies across borrower segments and economic conditions. A model trained on one lender’s data cannot generalize.

Why Better AI Alone Will Not Disrupt This

What if someone builds a better AI model?

The answer is that model quality alone does not win in this market. Even a significantly better model requires distribution (lending partners willing to integrate) and funding (institutional investors willing to buy the resulting loans). Pagaya has spent years building both.

A new entrant with superior AI would face the same chicken-and-egg problem that protects Pagaya from bank internalization. The moat is the system, not the algorithm.

The Funding Engine: How Capital Flows

The Pre-Funded Model Explained

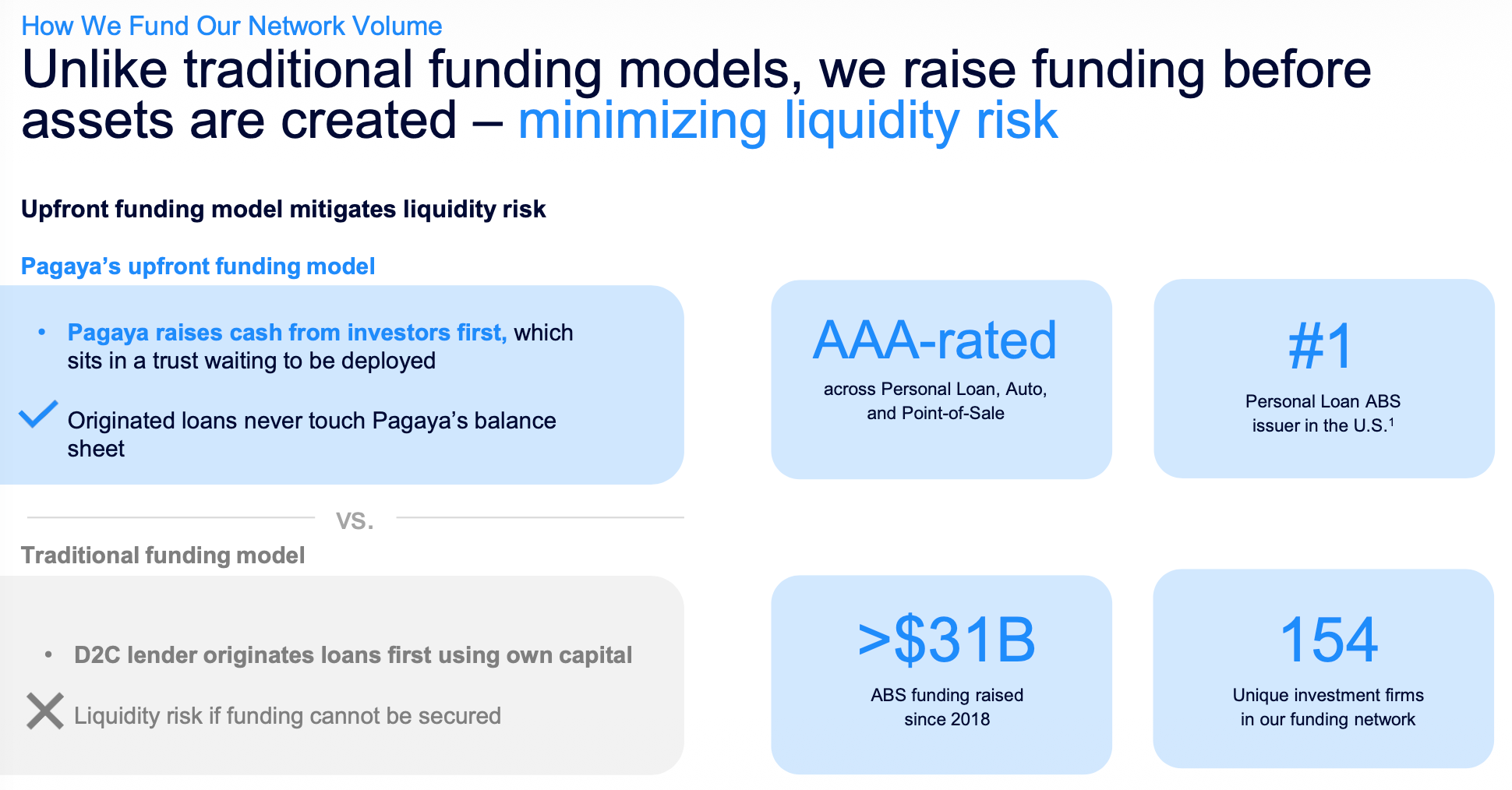

Most lenders originate loans first and then try to sell them. This creates a gap risk. If market conditions change between origination and sale, you are stuck holding loans you cannot sell at acceptable prices. This is exactly what crushed Upstart in 2022.

Pagaya inverts this model. It raises capital first and deploys it into pre-structured vehicles that buy loans as they are originated. Funding is committed before loans exist, eliminating any gap risk.

This is a fundamental structural advantage. When credit markets seize up, Pagaya keeps operating because its funding is already locked in. Competitors who depend on continuous secondary market access face existential pressure.

Three Funding Channels

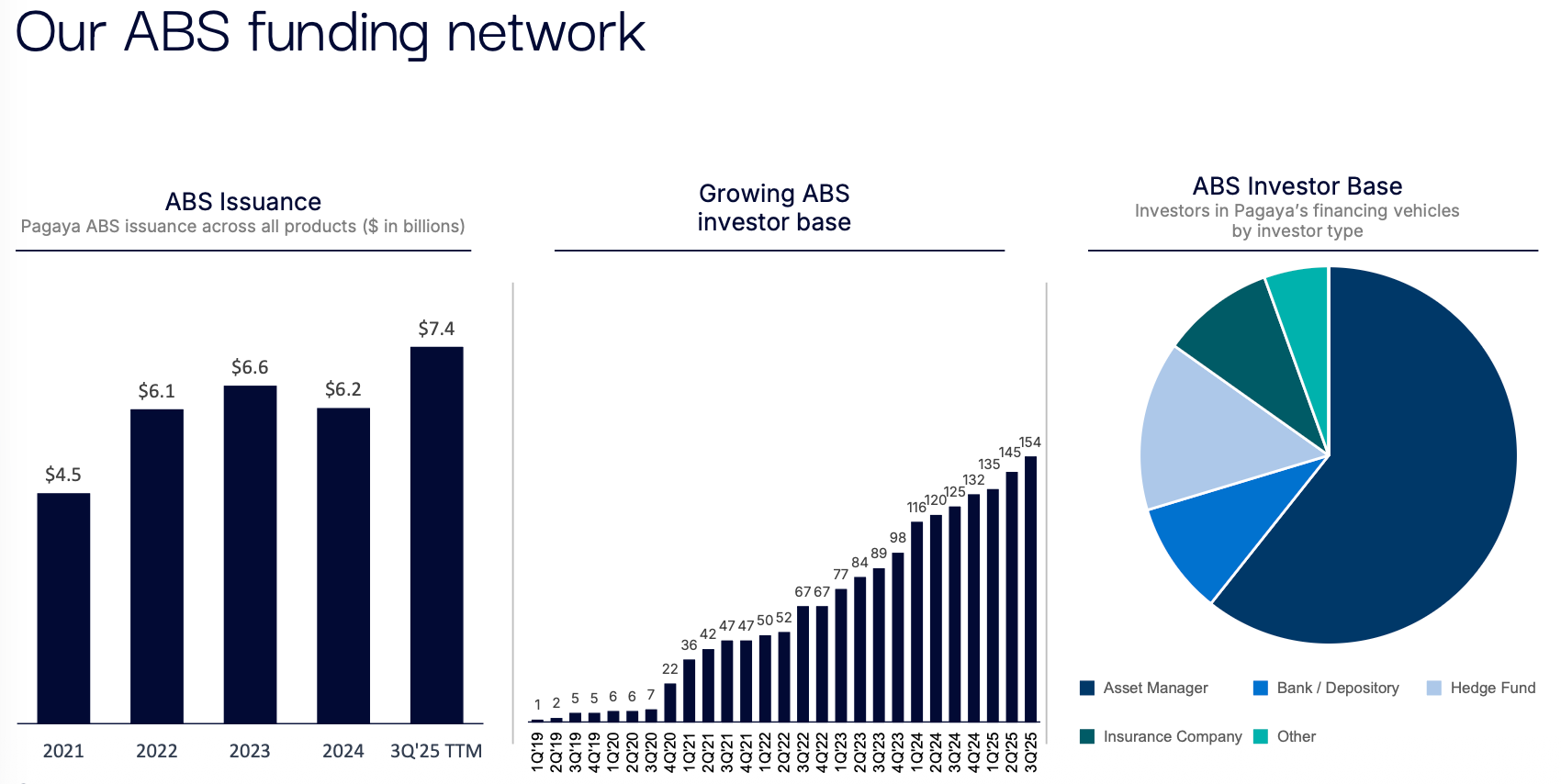

Asset-Backed Securities (ABS): Pagaya has issued over $34 billion across 83 ABS transactions since 2018, making it the #1 US personal loan ABS issuer. The company has achieved AAA ratings across its PAID (personal loan), RPM (auto), and POSH (point-of-sale) platforms. In Q2 2025 alone, it raised $2.3 billion across six transactions, attracting 74 unique investors.

Forward-Flow Agreements: Committed purchase agreements with institutional investors provide funding capacity outside ABS windows. Blue Owl’s $2.4 billion commitment and Castlelake’s $500 million auto agreement represent over $5 billion in forward-flow capacity.

Pass-Through and Revolving Facilities: The POSH shelf includes a revolving feature that recycles repayments into new loans, creating over $1 billion in effective funding capacity without additional securitizations.

Understanding the Risk Types

Liquidity risk (funding becomes unavailable) is minimized by the pre-funded model. Capital is committed before loans exist.

Credit risk (borrowers default) is transferred to ABS investors who purchase senior tranches. Pagaya retains only the 3-5% equity slice required by Dodd-Frank risk retention rules.

Balance sheet risk (mark-to-market losses on retained positions) exists, but is bounded. FRLPC now substantially exceeds retention exposure, meaning fee income covers any credit impairments.

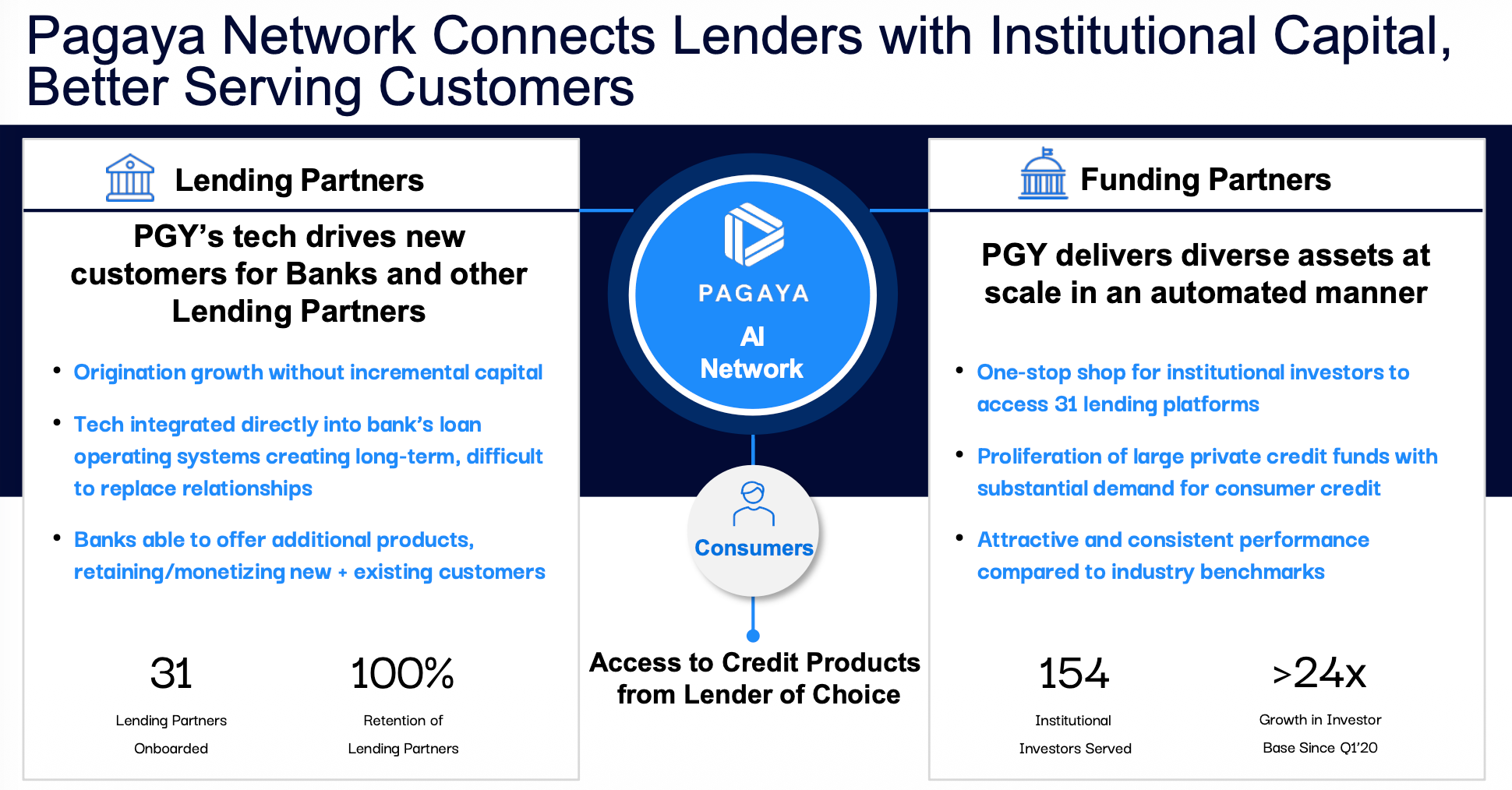

The Partnership Network

Current Partners and Growth Trajectory

Pagaya currently works with 31 lending partners, including major institutions like US Bank, SoFi, and Klarna. The company targets 1-2 new partners a year, with a third of the current pipeline consisting of regional banks entering AI-powered lending for the first time.

In August 2025, Pagaya joined the American Bankers Association Partner Network, a significant credibility signal that validates the company’s approach with traditional banking institutions.

How Partnerships Work

Pagaya integrations are deep technical embeddings, not the average vendor relationship. When a partner integrates Pagaya, they connect their loan origination system to Pagaya’s API. Applications declined by the partner’s own models flow to Pagaya for re-evaluation in real time.

This integration typically takes 12-18 months from initial engagement to meaningful volume. Partners must modify origination systems, establish legal frameworks, train operations teams, and pass compliance reviews. This complexity creates significant switching costs.

The Three Switching Costs

Operational: Switching requires re-engineering origination systems, re-training staff, and managing parallel workflows. Most partners have IT roadmaps planned years ahead.

Regulatory: Partners in regulated industries must ensure new vendors meet compliance requirements. A switch requires fresh regulatory review.

Reputational: Partners stake their customer experience on Pagaya’s underwriting quality. A switch that increased defaults would damage the partner’s brand.

The result? 100% partner retention rate since inception. Multi-product partners (using Pagaya across multiple asset classes) represent 30% of partner count but generate over 66% of volume.

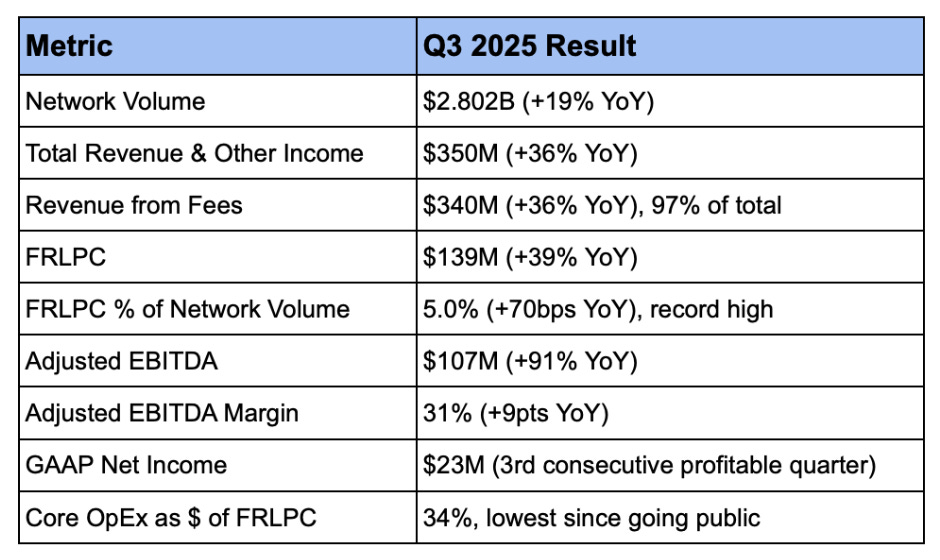

Financial Performance

Q3 2025 Results:

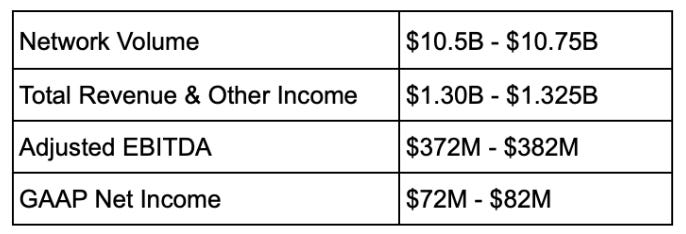

FY 2025 Guidance (Raised for Third Consecutive Quarter):

Credit Performance

Understanding Vintage Analysis

A “vintage” is a group of loans originated in a specific time period (Ex: “Q3 2023 vintage” means all loans originated in Q3 2023). “Cumulative Net Losses” (CNLs) measure the total percentage of loans that defaulted minus recoveries. “Month-on-Book” (MOB) is simply how the old loans are (Ex: MOB 12 means the loans are 12 months old).

Why does MOB matter? Loans default at different rates depending on their age. Most consumer loan defaults happen between months 6-18. By comparing CNLs at the same MOB across vintages, we get an apples-to-apples comparison of credit quality. If 2023 loans have lower CNLs at MOB 17 than 2021 loans did at MOB 17, that’s a direct signal that 2023 underwriting was tighter.

Data Sources

The credit performance data comes from three primary sources:

Pagaya’s Quarterly Earnings Supplements, which include vintage-level CNL charts tracking performance by quarter of origination

Management Commentary on Quarterly Earnings Calls

Pagaya’s Shareholder Letters

The Q3 2025 data referenced below comes from the November 2025 shareholder letter and earnings supplement, reflecting loan performance through September 30, 2025.

Personal Loan Credit Performance

The benchmark for personal credit is Q4 2021, the worst-performing vintage in Pagaya’s history. This was the peak of post-COVID credit stress. Here’s how more recent vintages compare at the same loan age:

2024 quarterly vintages (Q1-Q4 2024): CNLs are trending 35-40% lower than Q4 2021 peak levels at MOB 8-17. This means loans originated throughout 2024 are defaulting at roughly one-third lower rates than the worst vintage.

Second half 2023 and first half 2024 vintages: CNLs are trending 30-40% lower than Q4 2021 at MOB 11-20.

This tells us Pagaya’s AI underwriting has meaningfully improved. The company is approving higher-quality borrowers today than it did during the stress period.

Auto Loan Credit Performance

For auto loans, the benchmark is 2022 vintages (the peak stress period for subprime auto). Comparing recent performance:

2024 quarterly vintages (Q1-Q4 2024): CNLs are trending 50-65% lower than comparable 2022 periods at MOB 9-18. Auto credit performance is drastically better than during the stress period.

Second half 2023 and first half 2024 vintages: CNLs are trending 30-60% lower than comparable 2022 periods at MOB 11-20.

This tells us auto performance has improved even more than personal loans. This is particularly notable because auto investors demanded premium returns in 2022-2023 due to elevated losses across the subprime auto sector.

The 2023 Vintage Impairment

In Q4 2024, Pagaya recorded $229 million in credit-related fair value adjustments, with approximately 90% tied to vintages from 2023 and earlier. This requires some context to understand.

The 2023 vintages were issued during a brutal funding environment. ABS investors demanded yields of 15%+ to buy subordinate tranches because credit markets were stressed. When you structure a deal with such high required returns, the math becomes unforgiving. Even small changes in default rates can wipe out the equity tranche’s value.

The main takeaway is that the 2023 vintage loans actually performed well. As shown above, their CNLs are 20-40% better than 2021 peak levels. The impairments were not a credit quality problem, they were a deal structure problem. The high cost of capital baked into those deals left no margin for error.

Think of it like buying a house with a 15% mortgage rate. Even if the house holds its value, the economics are painful. The house isn’t bad, but the financing terms were just expensive.

Where We Are Now

As of Q3 2025, fair value adjustments have normalized dramatically. From the Q3 2025 Earnings Supplement:

Total fair value impairment in Q3 2025: $32 million (net of non-controlling interest), broken down as: 2023 & prior vintages: $1 million, 2024 vintages: $8 million, 2025 vintages: $1 million gain, Capitalized expenses (OCI): $24 million.

Compare this to Q4 2024’s $156 million in fair value impairments. The 2023 vintage write-downs are essentially complete. Management indicated on the Q4 2024 earnings that “the majority of any remaining impairments for that vintage” would be recognized by year-end 2024.

Today’s ABS transactions are priced at much tighter spreads (lower required yields). The company has achieved AAA ratings across all three ABS platforms (PAID for personal loans, RPM for auto, POSH for point-of-sale). A lower cost of capital means a greater cushion against credit fluctuations (deal structures are fundamentally more resilient).

Third Party Validation

KBRA (Kroll Bond Rating Agency) is one of the major credit rating agencies in the United States, registered with the SEC as a Nationally Recognized Statistical Rating Organization (NRSRO). Their job is to analyze asset-backed securities and assign credit ratings that institutional investors rely on when deciding whether to buy bonds. Unlike equity analysts, who might have investment-banking relationships or stock positions, rating agencies are paid to be skeptical. Their reputation depends on accurate credit assessment, not on whether a company’s stock goes up.

What makes KBRA’s analysis valuable here is access. They review actual loan-level performance data, including individual borrower payment histories, default rates, recovery amounts, and how cash flows through the ABS waterfall structures. This is granular data that short sellers, when comparing aggregate delinquency charts, simply don’t have. When KBRA says credit enhancement is increasing on a deal, they’re looking at the actual numbers, not making inferences from public filings.

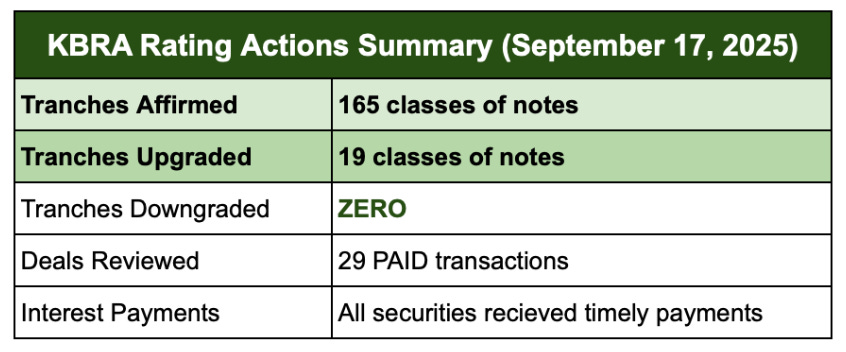

KBRA September 2025 Surveillance Review

On September 17, 2025, KBRA completed a comprehensive surveillance review of 29 Pagaya AI Debt Selection Trust and Pagaya AI Debt Trust (“PAID”) transactions. The data used was as of the August 2025 distribution date (July 2025 collection period). The results demonstrate strengthening credit performance across the portfolio:

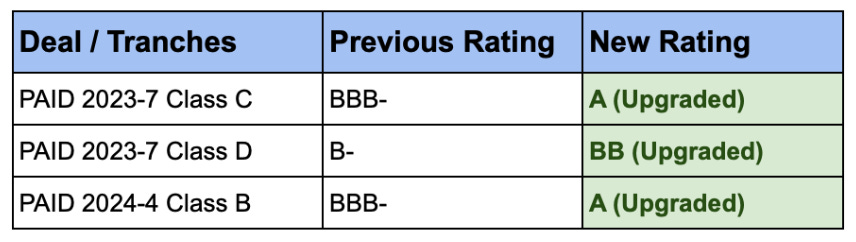

2023 Vintage Upgrades: The Bear Case Refutal

The most significant finding is that the same 2023 vintages that bear cases cite as problematic are receiving rating UPGRADES, not downgrades. This directly contradicts the thesis that 2024 delinquency rates similar to 2023 will produce similar impairments:

KBRA Key Findings (Direct Quotes)

"Existing credit enhancement for the notes is sufficient to support the revised and affirmed ratings."

"All of the securities with upgraded ratings experienced increased credit enhancement."

"To date, the securities have received timely interest payments."

Early Redemptions: Performance Exceeds Expectations

Multiple legacy deals (2021-2023) are being called or redeemed early via optional redemption mechanisms. For example, KBRA withdrew ratings on PAID 2023-5 in November 2025 following the exercise of optional redemption for all $792 million in outstanding notes. Early redemptions indicate that collateral performance exceeded note balances, allowing clean exits.

Sponsor Financial Stability (KBRA Assessment)

KBRA validated Pagaya’s financial position as of June 30, 2025:

$183 million cash

$468 million total shareholders’ equity

$413 million credit facility capacity

$6 billion in forward flow commitments

Diversified loan sourcing from Prosper, LendingClub, Upgrade, Avant, Marlette, SoFi, Rocket Loans, Cross River Bank, and US Bank. Backup servicing from Vervent Inc. and Systems & Services Technologies Inc. to mitigate servicing disruption risk.

Empirical Evidence vs. Chart Analysis

Rating agencies have access to actual loan-level performance data, loss severity curves, and enhancement waterfall models that short sellers, who rely on aggregate delinquency charts, do not. The fact that an independent third party with this granular data is upgrading tranches and finding increasing credit enhancement across seasoned deals provides empirical evidence that trumps surface-level comparisons of headline delinquency metrics.

The bear thesis that “2024 delinquency rates similar to 2023 will produce similar impairments” misses the forest for the trees. Credit enhancement is building, not eroding, on seasoned deals, the exact opposite of what you’d expect if credit were deteriorating. The 2024-2025 deal structures were issued with significantly better enhancement levels than the stress-era 2023 deals, giving them far more cushion against losses. And perhaps most tellingly, the same 2023 vintages that bears cite as problematic are the ones receiving rating upgrades as they season.